US Dollar Index looks offered near 99.00, focus remains on Ukraine

- DXY trades on the defensive and challenges the 99.00 zone on Tuesday.

- Investors continue to look to geopolitics for near-term direction.

- Trade Balance, Wholesale Inventories next of note in the US docket.

The greenback now gives away part of the recent advance and returns to the vicinity of the 99.00 neighbourhood when gauged by the US Dollar Index (DXY).

US Dollar Index keeps looking to geopolitics

The index met a tough barrier in the area of recent cycle peaks around 99.30 amidst unabated geopolitical concerns surrounding the military conflict in Ukraine and hopes that further talks between both parties could pave the way to an end of the dispute. It is worth recalling than another round of talks is expected to take place on Thursday.

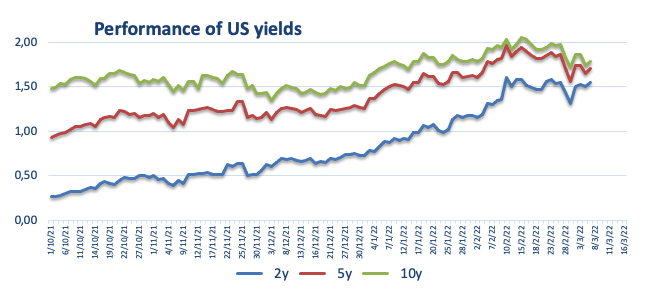

In the meantime, and following a tepid improvement in the risk-on sentiment, US yields add to Monday’s rebound across the curve, with the short end reaching monthly highs around 1.60%, the belly surpassing 1.80% and the long end trespassing the 2.20% level.

In the docket, Trade Balance results for the month of January will be in the limelight along with Wholesale Inventories. In addition, the NFIB Business Optimism Index is due followed by the IBD/TIPP Economic Optimism index.

What to look for around USD

The index clocked new cycle peaks beyond the 99.00 barrier at the beginning of the week, always in response to increasing geopolitical concerns in Ukraine. The persevering bias towards the safe haven universe is predicted to keep supporting the dollar and the rest of its peers in the current context for the time being. Also supportive of the stronger buck appears the current elevated inflation narrative, the start of the Fed’s normalization of its monetary conditions later this month and the solid performance of the US economy. In the longer run, the renewed hawkish views from the BoE and the ECB carry the potential to undermine the expected move higher in the dollar.

Key events in the US this week: Balance of Trade, Wholesale Inventories (Tuesday) – MBA Mortgage Applications (Wednesday) – CPI, Core CPI, Initial Claims, Monthly Budget Statement, Fed Quarterly Financial Accounts (Thursday) – Flash Consumer Sentiment (Friday).

Eminent issues on the back boiler: Escalating geopolitical effervescence vs. Russia and China. Fed’s rate path this year. US-China trade conflict under the Biden administration.

US Dollar Index relevant levels

Now, the index is losing 0.35% at 98.88 and a break above 99.41 (2022 high Mar.7) would open the door to 99.97 (high May 25 2020) and finally 100.00 (psychological mark). On the flip side, the next down barrier emerges at 97.73 (monthly high Feb.24) followed by 96.22 (55-day SMA) and then 95.67 (weekly low Feb.16).