US Dollar Index regains momentum and targets 93.00, US data eyed

- DXY reverses Tuesday’s pullback and advances to 92.80.

- US 10-year yields ease from tops and return to the 1.32% area.

- ADP Report, ISM Manufacturing next of relevance in the US docket.

The greenback, in terms of the US Dollar Index (DXY), manages to regain the smile and advance to the 92.80 zone early on Wednesday.

US Dollar Index now looks to data

After bottoming out in the 92.40 region on Tuesday, the index manages to regain buying interest and now re-shifts its attention to the key level at 93.00 the figure amidst higher US yields and some selling pressure in the risk complex.

In fact, yields of the US 10-year benchmark tested highs around 1.33%, just to ease some ground soon afterwards and managing well to keep business above the key 1.30% mark so far.

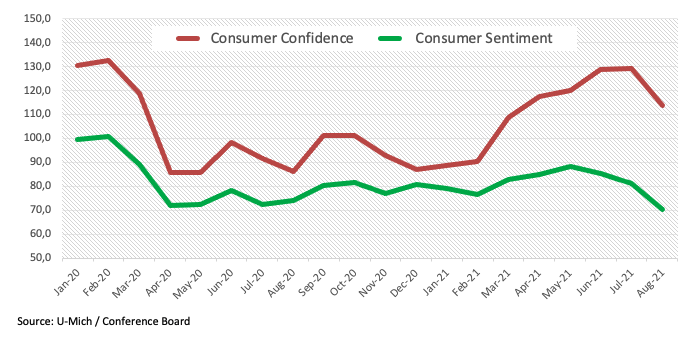

The dollar advances into the positive territory after inflation fears and COVID-19 concerns continue to weigh on the consumers’ behaviour, as noted by the recent decline in both prints of the U-Mich Index and the Conference Board’s Consumer Confidence.

Later in the US data space, the labour market will take centre stage in the first turn with the release of the ADP report for the month of August (613K exp.), while the critical ISM Manufacturing will be published later in the session (58.6 exp.) ahead of the weekly report on US crude oil inventories by the EIA.

What to look for around USD

Powell’s cautious tone at his speech at the Jackson Hole Symposium caught USD-bulls off guard, sponsoring a corrective move in DXY to multi-week lows around 92.40, where some decent contention turned up. In the meantime, support for the buck is expected to come in the form of coronavirus concerns, the uptrend in inflation and high real yields, while upcoming key data releases are predicted to have a crucial role in the timing of the start of the QE tapering.

Key events in the US this week: ADP report, ISM Manufacturing (Wednesday) – Balance of Trade, Initial Claims, Factory Orders (Thursday) – Nonfarm Payrolls, ISM Non-Manufacturing (Friday).

Eminent issues on the back boiler: Biden’s multi-billion plan to support infrastructure and families. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Debt ceiling debate. Geopolitical risks stemming from Afghanistan.

US Dollar Index relevant levels

Now, the index is gaining 0.08% at 92.71 and a break above 93.72 (2021 high Aug.20) would open the door to 94.00 (round level) and then 94.30 (monthly high Nov.4 2020). On the other hand, the next down barrier emerges at 92.40 (weekly low Aug.31) followed by 91.78 (monthly low Jul.30) and finally 91.61 (100-day SMA).