US Dollar Index loses momentum and drops to 2-day lows near 93.30

- DXY recedes to the 93.30 region at the beginning of the week.

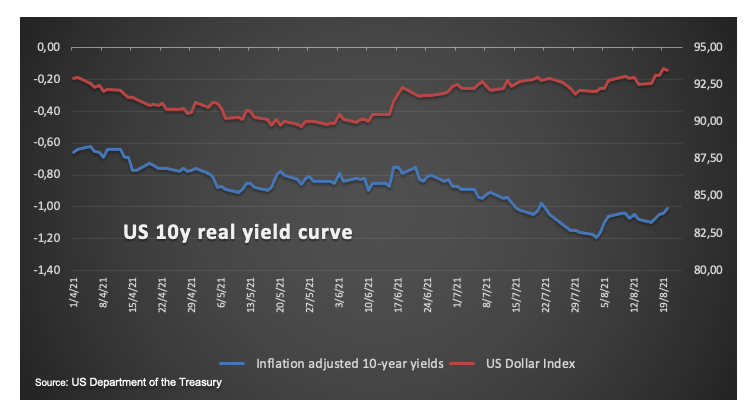

- US 10-year yields remain side-lined below the 1.30% level.

- The Chicago Fed Index, Flash PMIs, Existing Home Sales next in the docket.

The greenback, when gauged by the US Dollar Index (DXY), adds to Friday’s losses and re-visits the 93.30/25 band.

US Dollar Index focuses on data

The index so far loses ground for the second session in a row at the beginning of the week, although it manages well to keep business above the key 93.00 yardstick.

The dollar sparked a correction lower after reaching new 2021 tops in the 93.70 region on Friday. In fact, the now better note surrounding the risk universe puts the buck under pressure amidst the perseverant side-lined mood in US yields and despite ongoing concerns over the progress of the delta variant and the recent pick up in real yields.

Moving forward, further rangebound looks likely ahead of the critical Jackson Hole Symposium on August 26-28, where the QE tapering will take centre stage.

In the US data space, Markit wil publish its preliminary PMIs for the current month later in the NA session. In addition, Existing Home Sales are due followed by the Chicago Fed Index and the 3m/6m Bill Auctions.

What to look for around USD

After recording new 2021 highs in the 93.70 region last Friday, the dollar sparked a corrective downside and managed to abandon the overbought territory, as per the daily (RSI). The constructive performance of the dollar, in the meantime, has been further reinforced following the publication of the FOMC Minutes, where the Committee acknowledged that the QE tapering is closer than previously expected and the “sustained further progress” in the labour market still needs to be met in spite of the persistent economic recovery. Further support for the buck comes in the form of fresh coronavirus concerns, high inflation, higher real yields and the soft note in the risk complex.

Key events in the US this week: Advanced Markit Manufacturing PMI, Existing Home Sales (Monday) – New Home Sales (Tuesday) – Durable Goods Orders (Wednesday) – Flash Q2 GDP, Initial Claims (Thursday) – Jackson Hole Symposium, PCE, Personal Income/Spending, Advanced Goods Trade Balance, Final Consumer Sentiment (Friday).

Eminent issues on the back boiler: Biden’s multi-billion plan to support infrastructure and families. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Debt ceiling debate. Potential hint at the timing of QE tapering at the Jackson Hole Symposium. Geopolitical risks stemming from Afghanistan.

US Dollar Index relevant levels

Now, the index is losing 0.22% at 93.25 and faces the next support at 92.47 (low Aug.13) followed by 92.42 (50-day SMA) and finally 91.78 (monthly low Jul.30). On the other hand, a break above 93.72 (2021 high Aug.20) would open the door to 94.00 (round level) and then 94.30 (monthly high Nov.4 2020).